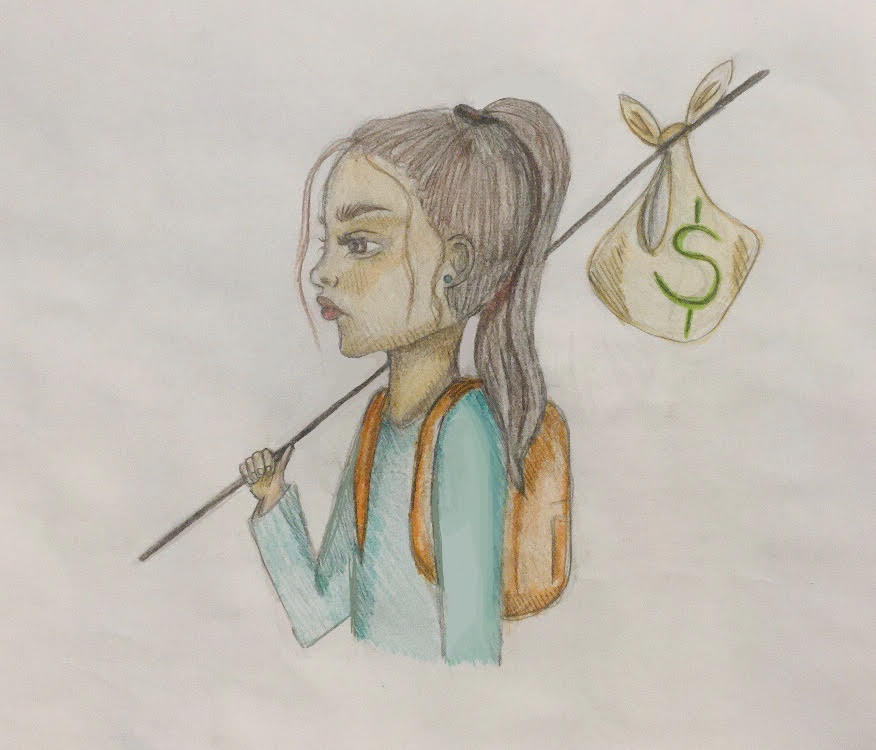

Do Kids Know Cash Like They Know Calc?

February 1, 2021

Across the US, from the affluent Wall Street investors, to the hopeful small business owners, one common aspect is required to reach prosperity. That is, money. The comprehension of finances can turn today’s startup businesses into tomorrow’s leading corporations. Yet, the same knowledge is needed to apply for a credit card or to resist from an online shopping splurge. Without this understanding, young adults can fall into the trap of credit, loan, and mortgage debts.

Unfortunately, less than half of the US population are estimated to pass basic financial literacy examinations. According to Thomas C. Corley, a CPA with a master’s degree in taxation, even wealthy individuals have encountered scenarios where they lose all their life’s savings, simply because of their lack of money management. Many millionaires are said to be cautious about small expenses, but manage to splurge on inappropriately priced cars, estates, and luxury items. Due to the lack of economic literacy and financial management skills provided by schools, anyone can lose their well-deserved wealth in only a few years worth of spending.

However, the lack of financial comprehension affects the working class on a much broader scale than it impacts the wealthy. Financial illiteracy can lead to problems like poor spending habits and weak savings. These can further lead to the inability of paying necessary bills, and can result in the early stages of bankruptcy.

The American educational system has excelled in academic subjects like: Science, Math, English, History, and World Languages. But are these subjects helpful when it comes to real life problems? Though one can not deny the fact that answering math problems can increase brain activity, solving for x is not necessarily useful when in need of filing tax returns.

Carle Place High School offers a financial elective instructed by Mrs. Foufas. Last semester she shared her concern about the widespread incomprehension regarding personal finances. For instance, the majority of Millennials are unaware of the dangers behind minimum payments; many do not even understand the idea of a “minimum payment”. These kinds of payments lead to a vicious cycle of debt and financial charges. Additionally, many high school seniors may be unfamiliar with the rather significant process of filing tax returns. This is mainly because financial classes are often offered as electives, rather than as an academic requirement. The optionality in financial literacy courses leaves many students feeling unaware of their economic responsibilities, especially after graduating high school.

Furthermore, some argue that financial independence and literacy can be taught at home. However, according to a survey in 2017, 69% of parents have reluctance about discussing finances with their children. School administrators expect high school students to receive financial knowledge from their family, whereas parents rely on schools to educate their children regarding this matter. Consequently, teenagers and Millennials are left on their own to manage their money. This often leads to huge piles of student debt.

According to Federal Reserves, in 2020, Americans owed more than $1.7 trillion in student loans. This amount is anticipated to increase as more students enroll in colleges. One reason for this unfortunate occurrence is the lack of knowledge pertaining to college expenses. For instance, many students would rather choose a reputable university, which costs twice as much as a public university, for the exact education. Many believe that the college one attends determines their career and overall future. However, this is not the case. According to Time Magazine, “Whether your degree, for example, is from UCLA or from less prestigious Sonoma State matters far less than your academic performance and the skills you can show employers.” Regardless, Millennials continue to attend prestigious colleges despite its cost. School debt can be prevented by educating students about expenses and real life financial challenges from a young age.

Champlain College enunciates, “Personal finance education should start early at both home and school. Ideally, personal finance concepts should be taught in elementary, middle and high school, and should continue into college.” Just as students learn math in an orderly academic structure, financial education should be taught in a similar manner. Instead of being offered as an elective course, which is more likely to be taken out of interest, financial literacy should be administered as a mandatory class. Beginning with defining money and its purpose, in an elementary level, the course can progress to tackling various financial scenarios in college-level case studies. For the reduction of debt, and the management of expenses, students deserve to know how to manage their money. After all, the knowledge of one year of Calculus may only last until finals, but a few years of Financial Literacy can be advantageous for a lifetime.

Bibliography:

Bernick, Michael. “Decision Time: It Doesn’t Matter Where You Go to College.” Time, Time, 10 Apr. 2014, time.com/54342/it-doesnt-matter-where-you-go-to-college/.

Corley, Thomas C. “I’ve Been a CPA for More than 30 Years, and Here Are the Top 6 Reasons Rich People Lose Their Money.” Business Insider, Business Insider, 20 June 2016, www.businessinsider.com/reasons-rich-people-lose-money-2016-6#-5.

“The Case for High School Financial Literacy.” The Case for High School Financial Literacy | High School Financial Literacy Report: Making the Grade 2017 | Center for Financial Literacy, Champlain College, www.champlain.edu/centers-of-experience/center-for-financial-literacy/report-national-high-school-financial-literacy/the-case-for-high-school-financial-literacy.

Hudson Hsieh • Feb 6, 2021 at 10:13 AM

Great article, this article was so professionally formatted and I was blown away by the quality of the writing.

It’s of paramount importance that students in high school learn how to manage personal finance and save for the future. By including real world statistics, you were able to paint a picture of how important it is for schools to educate their students on how to handle money and control debt, and conserve money for when they need it.